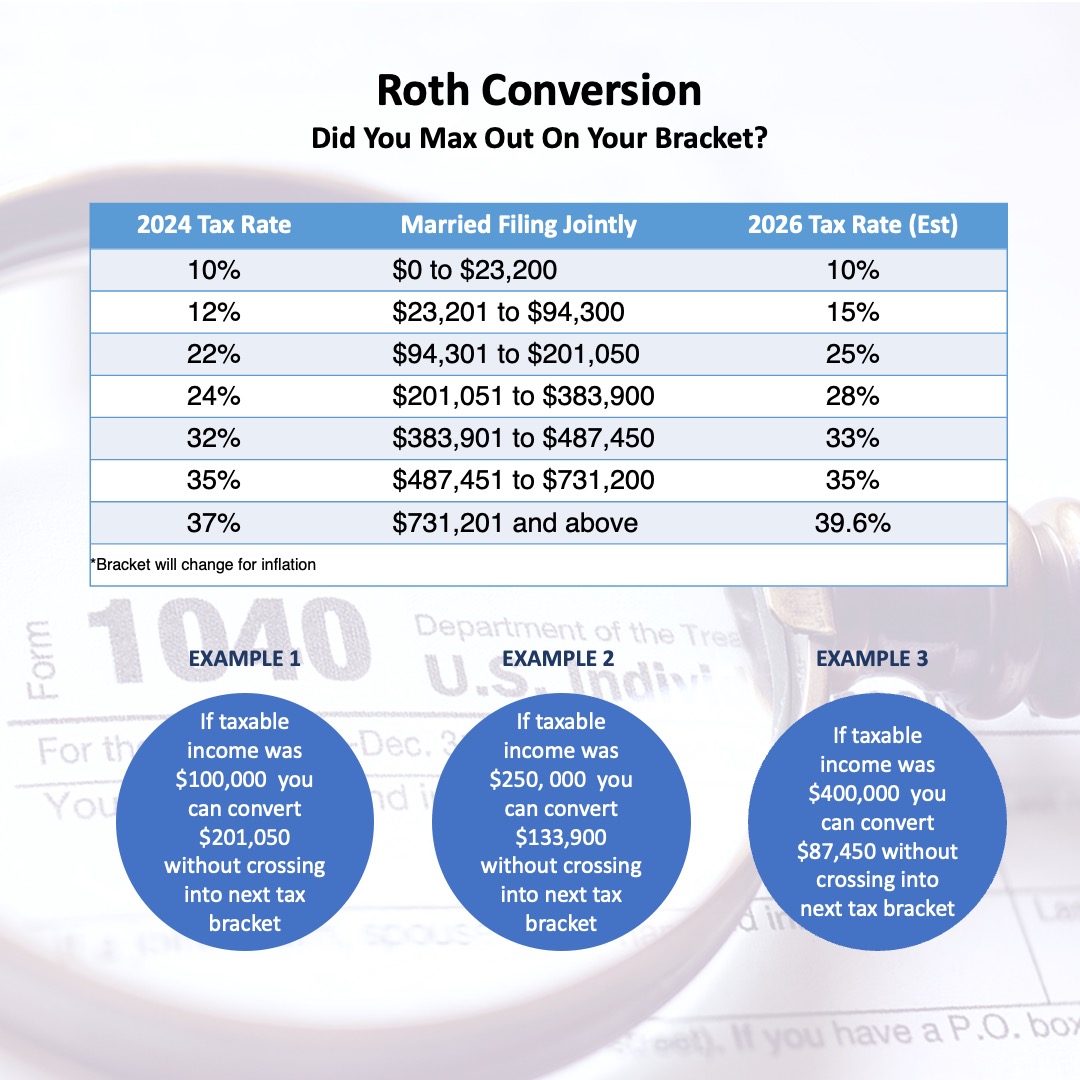

Maximizing your tax bracket with Roth conversions instead of waiting for the government to tell you how much you need to withdraw (RMD) can minimize your taxes in the long run. The longer you wait to convert, the larger your potential taxes can grow.

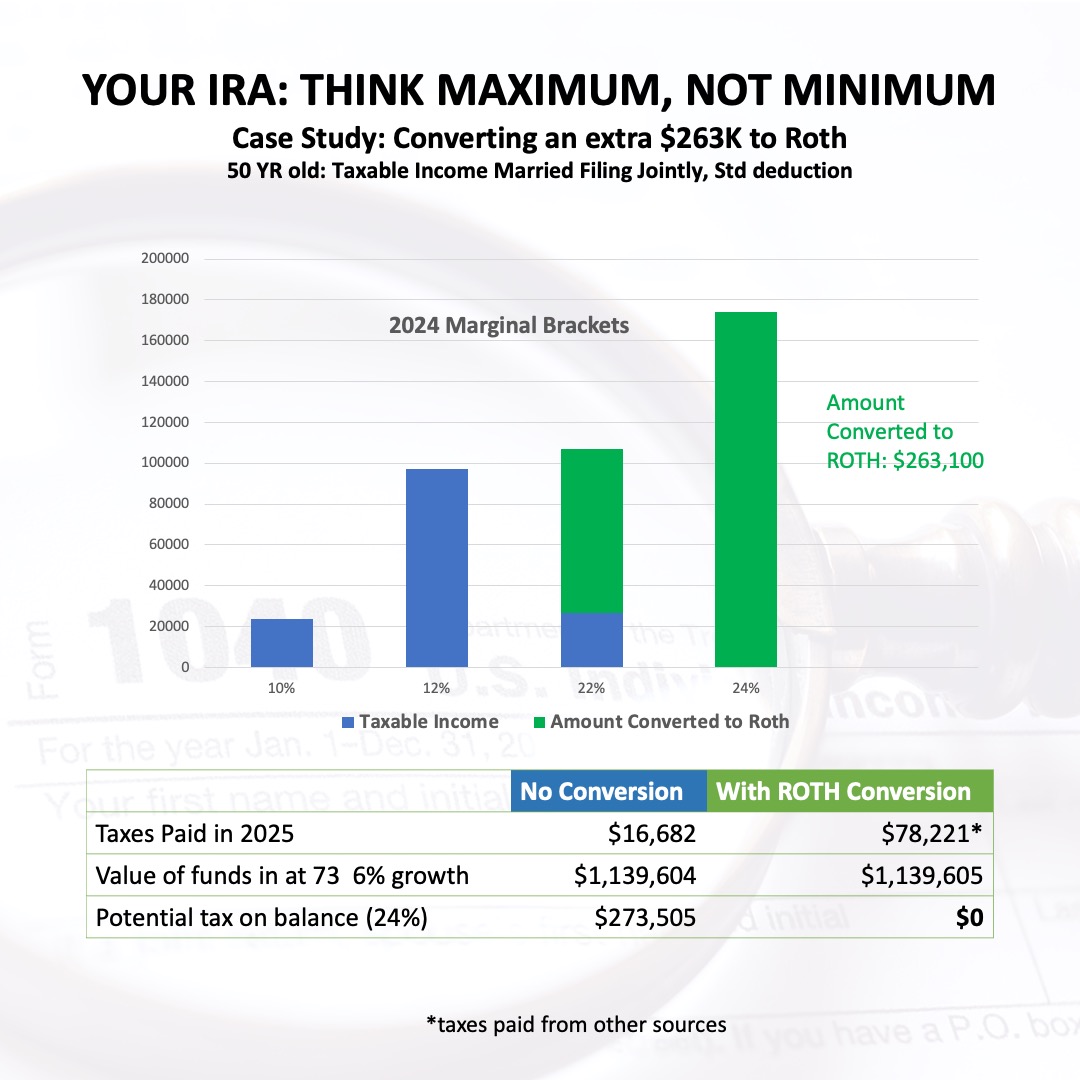

Take this example of a couple earning $150,000 a year. Before any conversions, their taxes paid will be $16,682. But this couple had some extra $$ and decided to fill up not only their 22% tax bracket, but convert a total of $263,100. They then paid a total of $78,221 in taxes.

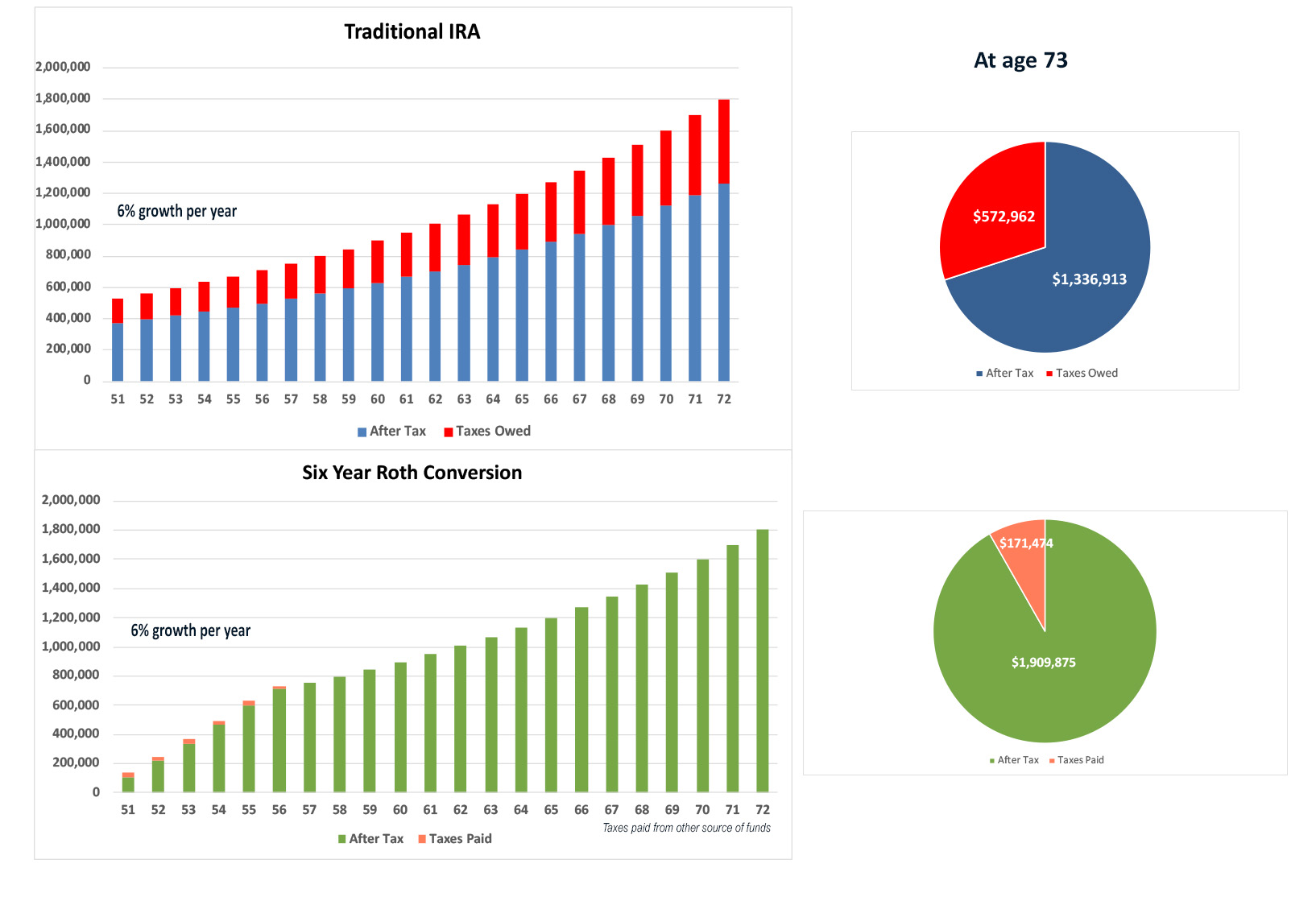

The $263,100 now enjoys tax free growth and withdrawals. Had they not done the conversion, their potential taxes at 24% would be $273,505, which is a great amount than the original principal. If Congress decides to let the rates from Tax Cut and Jobs Act expire, the current 24% tax bracket with go back to 28%, meaning you get to keep less of your hard earned money.

Waiting for RMDs is a passive approach that relinquishes control over your tax strategy.

By converting to ROTH strategically and maximize your tax brackets, you lock in lower tax rates, reduce or eliminate RMDs, and secure tax-free growth.

Maximizing tax free growth and minimizing taxes can have as much reward as picking the next investment winner. Consult a tax advisor for your personal situation to more accurately model your income and tax rates.